Why CRE is Underwriting Technology into New Deals

.webp)

Summary

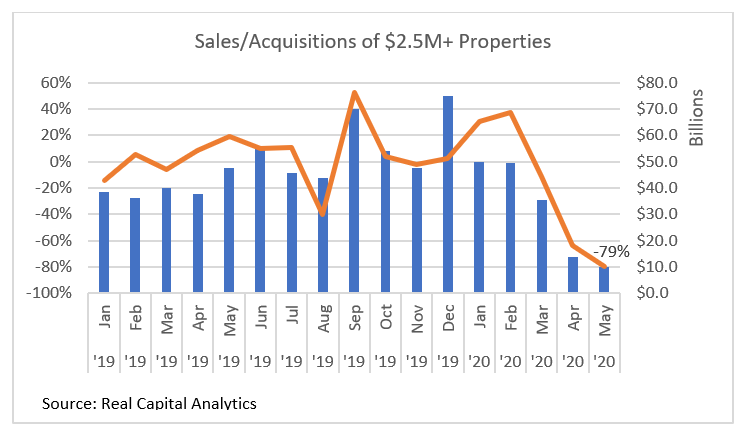

- The record $300 billion of dry powder to buy distressed assets is still on the sidelines despite the fall in values due to the coronavirus

- Investors are beginning to explore how technology can bolster their distressed fund strategy to help mitigate risk and maximize asset value

- Technology focused on cost savings can become a new tool in an investors arsenal

While no one saw a global pandemic coming, many commercial real estate investors have long believed that prices were too high and that the market was ready for a correction. As such, a whopping $300 billion of dry powder has lay ready to pounce for nearly two years.

And more is pouring in to buy distressed debt backed by hotels, malls, offices and other commercial properties suffering significant loses of value because of the coronavirus crisis. Kayne Anderson reportedly raised $1.3 billion for a new fund targeting distressed assets in only two weeks.

So far however, the powder has remained dry.

In fact, some investors believe that the true buying opportunities are still down the road. As Mitch Rosen from Yieldstreet put it, “With the public markets, you can drop 40 percent in three weeks, but real estate doesn’t work that way. The peaks and troughs are far longer in duration, and the distance between them is also much longer. I think the impact of what we see now is not going to be felt for six to nine months out, at least.”

Unlike the previous financial crisis, when some owners found themselves over leveraged and unable to meet debt obligations, the current economic crisis has undercut the basic theses of many investments. Most of the suffering has been concentrated in hospitality and retail, but larger demographic and cultural shifts are threatening the fundamentals of multifamily and office as well.

With lenders unwilling to throw good money after bad, investors are beginning to explore how technology can bolster their distressed fund strategy to help mitigate risk and maximize asset value.

New Underwriting Variables

One major problem in the current environment is that investors cannot accurately model a building’s cash flows over any time horizon because of the uncertainty around the continuing coronavirus crisis. Leases are in the processes of being renegotiated, historic renewal probabilities simply don’t apply, and rents are falling across most property types.

In addition, the unique nature of the pandemic creates added challenges in being able to conduct due diligence on assets or travel to sites to view properties. Moreover, the lack of deals means there’s no price discovery from the market.

Under these conditions, owners and asset managers are taking a closer look at the expense side of the pro forma. Long assumed to be fixed, better data is revealing that operating and capital expenses can vary significantly between similar assets depending on how each is operated. For investors looking to deploy dry powder as asset values fall, yet worried about future cash flow projections, granular cost data can reveal buying opportunities that would otherwise be missed.

For example, buildings with rampant inefficiencies may have hundreds of thousands of dollars of untapped net operating income available. Assuming these opportunities could be identified in the first place, how could an investor ensure that they capture this value as an owner-operator?

Including Technology in Initial Investment

Distressed fund investors were willing to wait for years for the market correction to take place because they wanted to purchase assets at a discount. However, under current conditions, it’s no longer sufficient to buy a distressed asset and continue the status quo. Even go-to strategies such as renovating the lobby and amenitizing the property will likely have no impact on cash flows in the short term.

To maximize asset value, investors should use part of that discount to invest in cost-saving technology. This does not mean blindly installing a building management system, which can cost anywhere from $2.50 to $8.00 per square foot. This means getting mobile apps that digitize documentation, assets, and workflows in the hands of operators for one or two cents per square foot.

This accomplishes three things. First, this is a low-cost first step that can be implemented (literally) on day one in any property type, making it easy to standardize across diverse investments. Second, this simple digitization creates buy-in among operators and engineers, enabling them to implement low-hanging fruit optimizations without changing their standard processes. Finally, this provides a roadmap for high ROI investments to make in each asset.

To capture the full potential of NOI through cost savings, mobile apps alone will likely be insufficient. Real-time data will need to be captured and analyzed. To ensure ROI, the initial digitization step simultaneously highlights issue areas to focus the necessary investments on. This could be chronic elevator repairs, inefficient HVAC use, overtime pay for engineers to inspect for pipe leaks, or unrecovered utility costs from submetered tenants.

Correcting any one of these can add millions of dollars in asset value, but there’s no silver bullet. The trick is to do this at scale without having to overspend for tech that won’t be used or paying consultants to do a deep dive into every asset.

Gaining a Premium at Disposition

The name of the game is buying low and selling high. Assuming an investor identified a property that had more cash flow potential than assumed due to excessive waste in operating expenses and was able to capitalize on that insights with technology underwritten into the deal, the asset value delta isn’t captured until the property sells.

During disposition, one way to increase the sale value is to decrease the risk premium. Obviously, generating healthy cash flows will be critical. However, the digitization of an asset provides additional opportunities.

For example, part of this risk premium is to cover an event in which critical equipment like the boiler plant has a catastrophic failure shortly into the new ownership period. When there’s no data to work from, these events seem random and push up the risk premium. In reality, they are not random, they are the result of poor maintenance practices and can be reasonably predicted. Given that, a seller with a digitized asset can demonstrate that the likelihood of a major failure is diminished, thus lowering the risk premium and raising the sale price.

Conclusion

For the $300 billion of dry powder waiting to be unleashed, there only seem to be two options. One is to start buying high quality logistics and data center properties that are poised for growth in the coronavirus economy, yet already expensive.

The other is to wade into the growing pool of distressed assets. While both Class A and Class B/C properties are feeling the heat, Class A owners generally have strong cash positions and low debt leverage. On the other hand, Class B/C is largely “value add” driven, with many owners highly leveraged and dependent on rent growth. As rents start to fall, Class A will start to lease at Class B prices, meaning that many distressed asset buys will have an uphill battle.

This doesn’t mean that there will not be enormous opportunities to purchase Class B assets at a discount. But doing so requires thinking outside the box. Technology that produces cost savings in a scalable and universally applicable way can be a new tool in the modern investors arsenal.

Enertiv is built to digitize assets quickly and deliver deep cost savings with targeted solutions. Schedule a demo today!