The Compounding Value of Technology, Part V: Cost Avoidance

%252B(1)%252B(1).webp)

In the last edition of the Compounding Value series, we focused on energy savings.

Unlike the earlier articles on productivity, the value of energy savings is obvious. A property used to spend a certain amount on utilities. Now it spends less, the difference is the savings.

But that’s not where the story ends.

Due to investor and regulatory pressures, every dollar reduced on energy consumption is also money not spent on things like renewable energy or regulatory fines.

This applies even to triple net lease portfolios, which do not pay much in utilities, and yet are increasingly held accountable for the emissions in their buildings.

In an era where environmental sustainability is not just encouraged but increasingly mandated, the value of energy efficiency must be recalculated to account for additional cost avoidance.

Regulatory Fines

For the past decade, cities and states have been passing regulations requiring building owners to provide energy benchmarking data.

To date, these mandates have been passed in over 45 cities, ranging from Columbus, OH to San Diego, CA. Massachusetts, Maryland, Minnesota, Colorado, Washington, Oregon and California have passed statewide mandates.

In 2019, New York City’s Local Law 97 set the bar for leveraging this data to pass strict emissions reductions requirements. Since then, eight more cities have followed suit, as well as the states of Washington, Oregon, Colorado and Maryland.

Legislation is under debate in countless additional jurisdictions.

Building owners have understandably been frustrated. A significant part of their ability to reduce carbon emissions is related to the relative emissions associated with generating electricity in the local power grid.

Nevertheless, like everything related to sustainability, the equation is not binary. It is not a question of going net zero or doing nothing. It is a question of whether, when regulatory fines are taken into account, there is a strong business case for energy reductions and renewable energy.

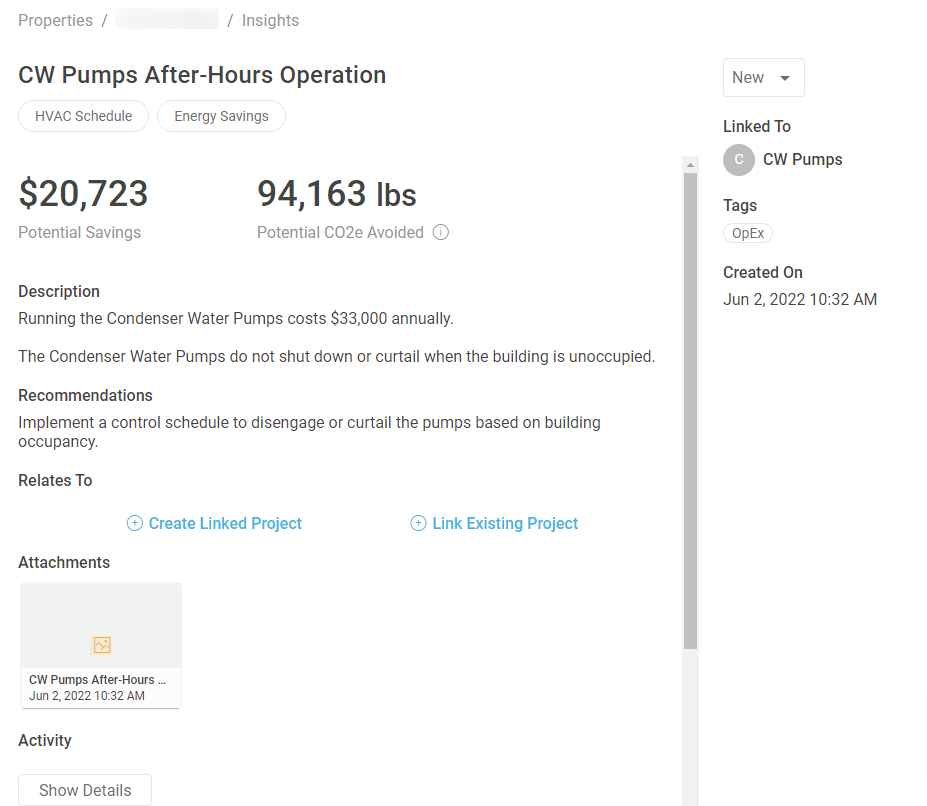

Let’s take this basic example.

This is an energy saving insight for a property in New York City that is currently operating above the emissions threshold.

There are $20,723 worth of direct energy savings annually.

That energy reduction equates to 94,163 lbs of CO2 per year, or approximately 47 tons.

At the current penalty of $268 per ton in New York City, implementing this insight adds another $12,596 worth of savings, a 38% increase on the total value.

Renewable Energy

Energy efficiency cannot get a building to net zero. Renewable energy, whether deployed directly or purchased, will have to be part of the equation.

But doing so comes at a cost.

Renewable Energy Credits (RECs) have long been a go-to product for companies looking to satisfy renewable energy goals and carbon reduction metrics.

Historically, RECs have been an appealing option due to the low cost and ease of purchasing compared to more complex, and often capital-intensive, renewable energy projects such as onsite solar.

However, over the past 18 months, the cost of a Green-e Certified REC has risen from roughly $1 per REC to almost $8 per REC. Just two years ago, the same RECs were selling at closer to $0.50 each.

One REC equates to one megawatt-hour (MWh). The insight above represents about 70 MWh worth of reductions. At $8 per REC, which adds another $562 to the value of the insight.

The REC example might only be a 2.6% increase on the total value but extrapolated across an entire portfolio would be a significant sum.

While the cost of deploying solar directly is not as volatile as the REC marketplace (costs have steadily decreased over time), it does also come with project management complexity.

Conclusion

As regulations become stricter and investor pressures on sustainability grow, the value of energy efficiency will only increase. The sharp increase in the cost of RECs are a perfect example of this, as demand has rapidly outpaced supply.

In this article, we found that every dollar saved on energy reductions translates to $1.40 when we take into account regulatory fines and/or purchasing renewable energy.

As the Compounding Value series takes shape, the bigger picture is becoming more clear.

From the humble beginnings of time savings, to the marginal gains through tech consolidation, the stage has been set for bottom line value.

The previous two articles covered the value of utility recovery from tenants and direct energy savings. What this article begins to uncover is that taking in a broader lens allows for the true value of technology to be realized.

The following articles will explore additional types of direct savings in the form of repairs, property damage and deferred CapEx.

While obviously valuable for cash flows and NOI, the goal will be to continue to expand our lends to understand the impacts on leasing, accessing capital and increasing asset value at disposition.